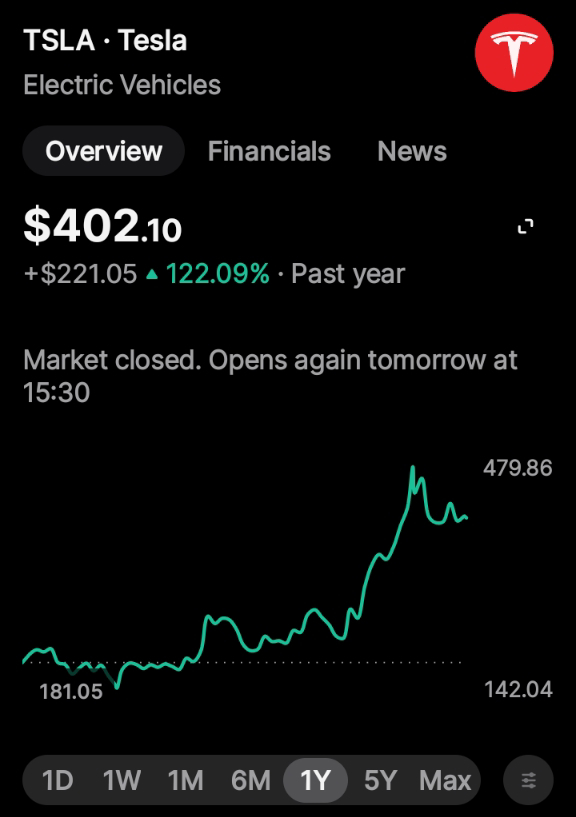

Tesla reported weaker-than-estimated Q4 2024 results, but the stock received a boost due to the promise of more affordable vehicles.

Key Figures vs. Bloomberg Consensus:

Revenues: $25,707 million (+2% YoY) vs. $25,200 million estimate.

EBIT: $1,583 million (-23%) vs. $2,670 million.

EPS: $0.66 (-71% YoY) vs. estimated $0.67.

Analysis of Tesla's Results: Disappointing Performance

Tesla's Q4 2024 results were weak and fell short of estimates. Demand weakened, leading to a -1.1% drop in deliveries (to 1.78 million units) for the full year. The company's strategy to increase volume involves maintaining discounts and financing facilities, which has negatively impacted margins. The gross margin for the auto business closed the quarter at 16.6% vs. the estimated 18.9%, aligning with the margin achieved in Q4 2023. Excluding regulatory loans, the margin was 13.6% vs. an estimated 16.2% and 14.8% in Q4 2023. In Q3 2024, it reached 17.0%. Despite these challenges, the stock rose +4% in aftermarket trading.

CEO Musk's Comments on Future Plans

During the conference call with analysts, Elon Musk, CEO of Tesla, highlighted several key points for the company this year:

- Affordable Model Launch: Musk reiterated plans to launch a more affordable model in the first half of the year.

- Autonomous Vehicle Service: He also announced the launch of an autonomous vehicle service by June but did not provide details on how this service will operate or specifics about the new models' cost, size, or design. Additionally, he did not comment on delivery growth guidance for the year. In Q3, Tesla set a target of +20%/+30% growth by 2025, which is ambitious given the weakening demand for electric vehicles and increasing competition in key markets like China (approximately 25% of revenues). In the US (50% of total sales), purchase subsidies are also under scrutiny. Consensus estimates suggest deliveries will reach 2.07 million units, equivalent to +16% YoY growth. Trump's victory in the US elections has been a strong support for Tesla's stock due to speculation about favorable regulations for the company, given Musk's support and closeness to the new President.

Market Sentiment and Execution Risk

Despite market optimism, Tesla's operations are facing significant challenges, as evidenced by these financial figures. At current share price levels (P/E 2025e 121x), the stock incorporates demanding estimates for both deliveries and autonomous driving development (robotaxi). We consider the execution risk to be high given these factors and advise caution moving forward.

Comments

Post a Comment