The bond sell-off seems to be moderating slightly (Bund 2.52% T-Note 4.66%), but yields are still too high for stocks to advance. Yesterday, they just flattened, distracted and worried about US employment data to be released tomorrow, which is likely to be stronger than desired, which would push the Fed away from cutting rates... which would favor bond yields not giving in. That is the main obstacle. However, surprisingly, the ADP Private Employment Survey came out somewhat weak yesterday (122k vs 140k expected vs 146k previous). But tomorrow's employment figures (2:30 PM) are the decisive ones, by official figures. Payrolls or Non-Farm Payroll Creation of only 160k vs 227k previous, Private Employment 135k vs 194k, Unemployment Rate repeating at 4.2% and Wages also repeating at +4.0% are expected. These figures, rather weak, would be good for stocks to stabilize and try to rebound a bit because yields would relax somewhat. But it is advisable not to trust because it would be strange for employment in a December month, usually good due to seasonality, to come out weak.

The minutes of the Fed meeting on December 18th, released last night, express increased risks to inflation in the face of uncertainty about the policies that Trump may adopt. Normal. Reminder: 1 member (Cleveland) voted to maintain, but they agreed to lower -25pb, to 4.25/4.50%. There is already some internal dissent of a hawkish/hard approach. This morning, China has repeated inflation at +0.1%, which is like admitting that it cannot activate Private Consumption and that the economy is not growing much. The already known. Chinese stock market -3.9% so far in 2025, by the way. We insist: do not invest in China. The only "investable" emerging market now is India... and we'll see.

At 8 AM, German Industrial Production came out good (+1.5% m/m vs -0.4% previous), within the bad situation it is (-2.8% y/y vs -4.2%). It is the first good news of a dull day because NY WILL BE CLOSED for the funerals of former President Carter (who, by the way, returned the sovereignty of the Panama Canal: Carter-Torrijos agreements).

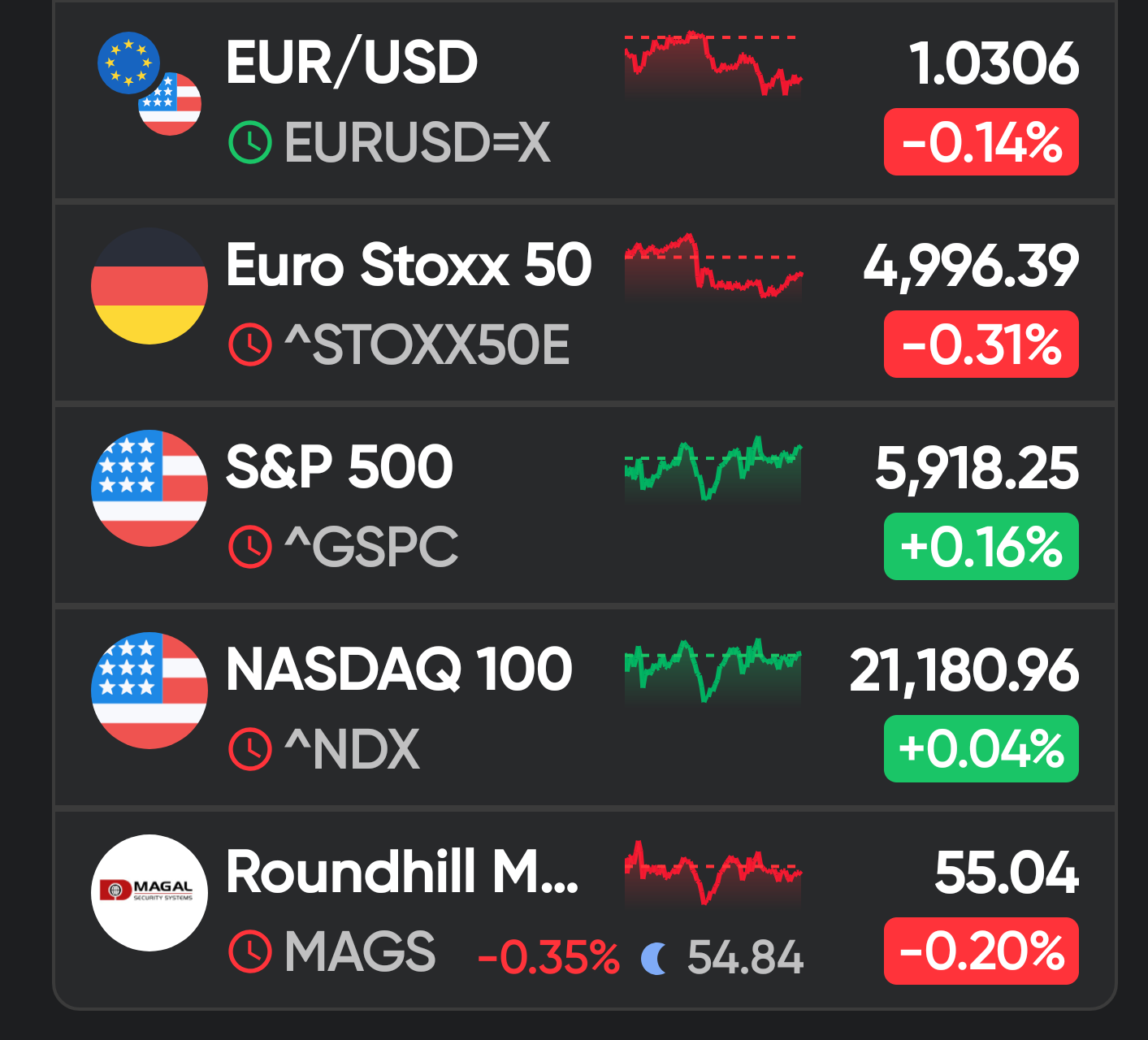

The only reference of the day is the UEM Retail Sales at 11 AM, which should come out decent, although not improving: +1.7% vs +1.9%. We cannot orient ourselves with that. Nothing to do until the American employment data comes out tomorrow. Meanwhile, TODAY Europe without daring to do anything, with NY closed and after mild declines in Asia this morning (ca.-0.3%). The most likely thing is that Europe will drip without attracting attention, but with a sad tone. The USD could appreciate to slightly beyond 1.03/€ (¿1.0295?) and bond yields could rise again somewhat because there are issues in France and Spain.

Comments

Post a Comment