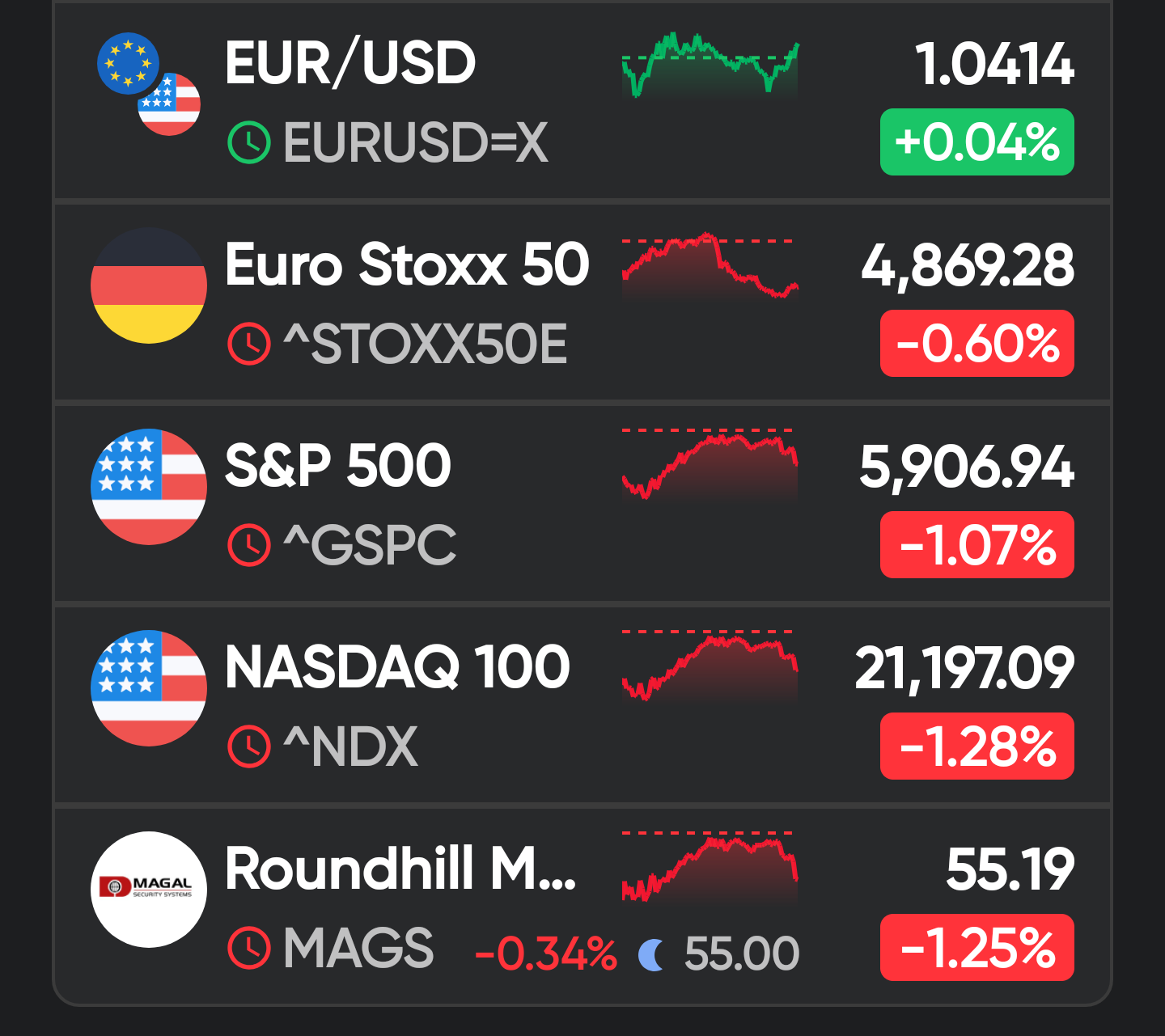

Wall Street opened sharply lower for no apparent reason, with exaggerated movements due to low volumes, dragging down a Europe that was pointing towards a rather flat close. In the absence of obvious culprits, attention turns to the T-Note yield. This loosens -9 bp to 4.54%, but Trump is at the door and, with inflationary policies, the fear of a rebound in bond yields causes some preventive profit-taking… and justified after the generous balances of the year, especially in American stocks (~+23%/+26%), Europe (+8%).

Macro, concentrated in the US, was mixed and second-tier (Chicago PMI bad, Housing Starts great and Dallas Fed manufacturing indicator very good). It went unnoticed because, by the time it was published, the markets had already gained downward momentum.

Today is a semi-holiday session in Europe, whose markets will close at midday (2 pm) and without any publications of interest. In the US, the day will run on its usual schedule and there will be references. The most relevant will be the Case-Shiller Home Prices, which will likely continue to expand slightly above +4% y/y, although they will reflect a moderation for the seventh consecutive month, which is consistent with an environment of higher interest rates for longer than initially estimated (30A mortgage rate, 6.75%). Early in the morning, China's December PMIs came out weak on the Manufacturing side (50.1 vs 50.3 previous) and slightly better on the Services side (52.2 vs 50.0 previous). They failed to cheer up the CSI300 in its last session of the year (-1.3%), although it achieves a positive annual balance for the first time since 2020 (~+15%).

Therefore, today we will have a session with few references, low trading volume and probably new downward drips. We reiterate that we must be cautious and expect less from the coming quarters, until the price adjustment is complete and inflation/rates clarify where they are going. Trump's measures and the political situation in relevant countries such as Germany are clarified. The natural thing will be for the markets to retreat a bit for a while, for bonds to continue to gently raise their yields, for the USD to remain appreciated (at some point in 2025 we will see parity with the euro), euro and yen weak, oil rather cheap and cryptos in a typical profit-taking of upside risks.

Happy 2025!

Comments

Post a Comment